Editor’s Note: Dr. Nicholas Spiro is managing director of Spiro Sovereign Strategy, a consultancy specializing in sovereign credit risk.

Story highlights

At the ECB meeting "Draghi had to walk a technical, political and legal tightrope"

"Draghi has placed the bond-buying ball firmly in the court of Madrid."

Today’s ECB press conference was always going to be about one thing, and one thing only: how the ECB intends to eliminate “convertibility risk” in the eurozone.

Although last month’s uptick in inflation was a key factor, the very fact that the ECB kept interest rates on hold amid a worsening of economic conditions across the eurozone shows the extent to which standard monetary policy measures have lost their effectiveness.

The bar was set extremely high for the ECB at today’s meeting and Mario Draghi had to walk a technical, political and legal tightrope.

It is noteworthy that Draghi began his presentation of the bond-buying program by underscoring the importance of strict conditionality.

The Outright Monetary Transactions (OMT) programme, if launched, will be heavily contingent on strict enforcement and external oversight of domestic policy reforms as part of an EFSF/ESM program. This is likely to make Madrid and, in particular, Rome wary of requesting such aid in the absence of severe market pressure.

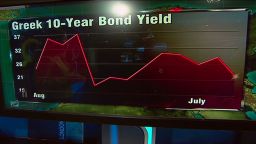

Draghi has placed the bond-buying ball firmly in the court of Madrid. The risk is that the credibility and effectiveness of the OMT program are undermined by doubts about the willingness of Spain to accept the conditions and adhere to them.

There is an inherent tension between a technical operation to repair monetary policy transmission channels in the eurozone and a heavily conditional aid program aimed mainly at two countries which are already resisting its conditions. The implementation risk of the OMT program is considerable.

Indeed favorable bond market reaction to Draghi’s OMT program will, paradoxically, delay its launch.

Last but by no means least, Draghi failed to specify how exactly the ECB intends to eliminate “convertibility risk”. This is not surprising given that the ECB itself is unsure about the precise determinants of sovereign spreads in the eurozone.